From Associate to Owner: How Long It Really Takes to Buy a Practice

Co-Founder, Minty Dental

The Two Timelines Most Buyers Confuse

When associates ask how long it takes to buy a practice, they're usually thinking about the wrong timeline. The transaction itself — from signed letter of intent to closing — typically takes 2-4 months. But that timeline only matters if you're ready to move when the right practice appears. The preparation phase — building liquidity, improving credit, assembling advisors — often takes 6-12 months and determines whether you can act at all.

What tends to happen: an associate sees a listing that checks every box. Strong patient base, solid financials, desirable location. They reach out, express interest, start imagining the transition. Then the lender asks for tax returns, a down payment estimate, proof of liquidity. The associate realizes they don't have 10-15% saved, their credit score sits below 700, they haven't spoken to a CPA in two years. The practice sells to someone else while they scramble.

The associates who close fastest aren't necessarily the ones with the most income — they're the ones who started preparing before they found a practice. They opened lender conversations six months out. They built relationships with a dental-specific CPA and attorney. They tracked their credit and addressed gaps. When a practice hit the market, they had pre-approval in hand and could move through due diligence without delays.

One pattern worth noting: buyers who treat preparation as optional often spend 12-18 months searching for practices they can't actually afford. Buyers who front-load the work compress their total timeline significantly — not because the transaction moves faster, but because they're ready to transact when the right opportunity appears.

The Preparation Phase: 6-12 Months Before You Make an Offer

The work that determines whether you can close starts months before you find a practice — building the financial foundation and professional relationships lenders require.

What Lenders Actually Evaluate

Banks financing dental acquisitions look at three core factors: credit history, liquidity, and clinical experience.

Credit score is the first filter. A score of 700+ positions you as a strong candidate with competitive rates. Scores between 650-699 are workable but may require explanation or limit lender options. Below 650 typically requires documented improvement before most banks move forward. If your score sits below target, six months of consistent payments and reduced credit utilization can shift the conversation.

Liquidity is where many buyers get surprised. Even with zero-down financing — which many dentists qualify for — lenders still want roughly 10% of the purchase price in cash reserves. For a $700,000 practice, that means $70,000 in accessible funds. This isn't money you'll necessarily spend — it's proof you can weather disruptions without defaulting.

Clinical experience matters more than most associates realize. Most lenders require at least one year post-graduation for general dentists before approving acquisition financing. Specialists may qualify immediately after residency, but timelines depend on the lender and practice complexity. If you're in your first year, that's not a reason to delay preparation — it's a reason to start building liquidity and relationships now.

Three Conversations to Start Early

The most valuable step you can take 6-12 months out is talking to lenders — plural. Reach out to at least three banks specializing in dental practice financing. These aren't applications. They're discovery calls where you learn what you qualify for, what gaps exist, and what timeline makes sense.

Many buyers avoid this because they assume they're not ready. That's backward. Lenders will tell you what to improve and how long it takes. Waiting until you find a practice means discovering gaps under pressure, often while competing against buyers with pre-approval.

Review your current employment agreement — specifically non-compete clauses. Some contracts restrict where you can practice within a certain radius or timeframe after leaving. If your agreement limits options, you need to know before touring practices.

The third conversation is assembling your advisory team: a dental-specific CPA, an attorney experienced in practice transitions, and a lender who understands dental acquisitions. These aren't people you hire the week before closing — they're relationships you build early. A strong CPA helps you understand what the financials actually mean. An experienced attorney catches risks a general business lawyer might miss. A lender who knows dental practices structures terms that align with your cash flow reality.

What This Phase Actually Looks Like

In practical terms: pull your credit report and address issues, open a dedicated savings account and automate transfers until you hit your liquidity target, schedule intro calls with three lenders and take notes, connect with a dental CPA and attorney even if you're not ready to hire them yet.

The buyers who move fastest once they find a practice treated this phase as foundation, not waiting room.

The Transaction Phase: What Happens Between LOI and Closing

Once you've found a practice and submitted an offer, the transaction moves through overlapping phases. The total timeline from signed letter of intent to closing typically runs 2-4 months, but speed depends on how prepared you are and how responsive both parties stay.

LOI Negotiation: 1-2 Weeks

The letter of intent outlines your proposed purchase price, basic terms, and contingencies. This stage typically takes one to two weeks. Delays happen when buyer and seller haven't aligned on fundamental terms before drafting — if your offer is significantly below expectations or if key deal points like transition support weren't discussed upfront, you'll spend extra time renegotiating.

One pattern: sellers genuinely ready to exit respond quickly and negotiate in good faith. Sellers who hesitate or counter aggressively on every point may not be as committed as their listing suggests. Pay attention to how this stage unfolds — it often signals how the rest will go.

Due Diligence: 2-4 Weeks

This is when you get access to details that matter: patient charts, detailed financials, equipment condition, operational systems. Most LOIs include a contingency period allowing you to walk away if you uncover deal-breakers — use it. Due diligence typically takes two to four weeks, though it stretches when seller records are incomplete.

What slows this phase: missing documentation. If the seller can't produce three years of P&L statements, patient retention data, or equipment maintenance records, you're either waiting or making decisions with incomplete information. Buyers who assembled their advisory team early move faster because their CPA and attorney know exactly what to request and how to interpret it.

Financing Approval: 2-4 Weeks (Often Overlapping)

While due diligence is underway, your lender works through underwriting. This typically takes two to four weeks and runs parallel to your review. Lenders need documentation, valuations, and credit committee approval before issuing a commitment letter.

Buyers lose time when they haven't organized personal financials or when the lender raises questions requiring additional documentation. If you started lender conversations during preparation, this step moves faster — your lender already knows your financial profile.

Contract Negotiation: 2-4 Weeks

Once due diligence is complete and financing approved, the purchase agreement gets drafted and negotiated. This adds two to four weeks, especially if terms shift based on what you uncovered. If equipment needs more work than expected or patient retention is lower than represented, you may renegotiate price or request seller-financed adjustments.

Buyers who close fastest work with attorneys specializing in dental transitions. A general business lawyer may take longer or miss industry-standard protections.

Third-Party Approvals: The Biggest Wildcard

The final phase involves approvals from parties outside the transaction. Lease assignments, licensing transfers, and credentialing with insurance panels all require third-party sign-off, and timelines vary widely.

Landlord consent is the most common delay. If the lease isn't assignable or the landlord is slow to respond, you may add weeks even after everything else is finalized. Some landlords require personal guarantees or renegotiate terms when ownership changes. Starting this conversation during due diligence helps surface issues before they become closing delays.

Licensing and credentialing timelines depend on your state and the insurance panels the practice participates with. In most cases, these processes run parallel to the transaction, but they can extend beyond closing if not initiated early.

The buyers who close in 60-75 days rather than 90-120 respond to requests immediately, keep their advisory team aligned, and started lender conversations months before they found a practice.

Building Your Financial Cushion: How Much Cash You Actually Need

The question most associates ask first: how much money needs to be in your bank account before you start looking at practices?

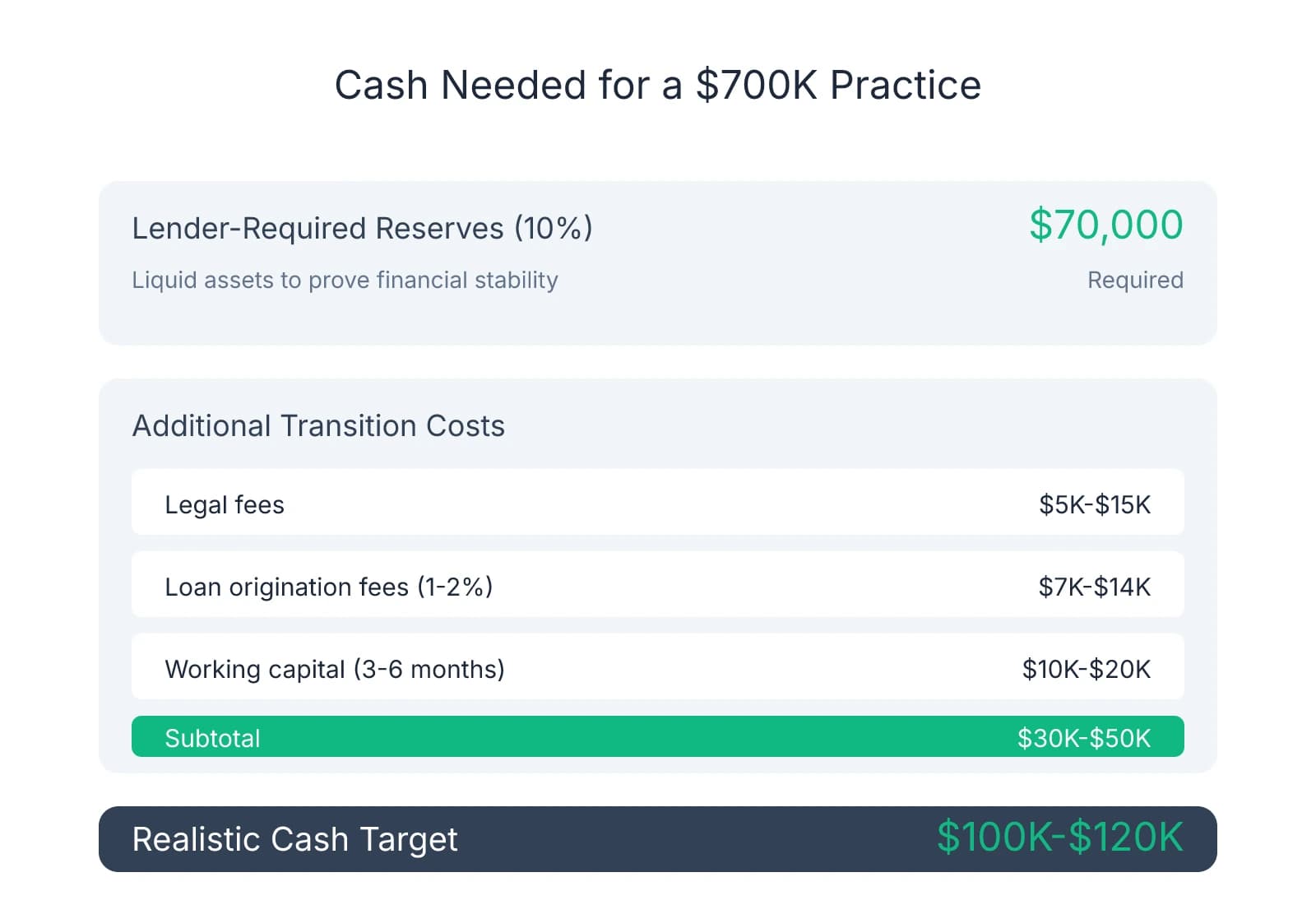

The answer splits into two numbers buyers often conflate. The first is what lenders require as proof of financial stability — typically 10% of the purchase price in liquid reserves. The second is what you actually need to cover costs and cash flow gaps that come with any ownership transition. Most lenders want at least 10% of the practice purchase price in accessible cash, even with zero-down financing. For a $700,000 practice, that means $70,000 in reserves.

But that $70,000 isn't the full picture. Zero-down financing is common for strong buyers, but it doesn't mean zero cash on hand. Lenders structure these deals because they want you to succeed — and they know that depleting liquidity with a large down payment leaves you vulnerable if revenue dips or unexpected costs appear in the first months. What they're protecting against: you close the deal, hit a slow month, and can't cover payroll or loan payments because you spent everything getting to the closing table.

What the 10% Reserve Requirement Actually Covers

When lenders ask for 10% in reserves, they're looking for liquid assets: cash in savings or checking, money market funds, or brokerage accounts with stocks and bonds you can access quickly. Retirement accounts don't count unless you're willing to take early withdrawal penalties. Home equity doesn't count. The bank wants money you can deploy immediately if the practice underperforms in the first six months.

This requirement exists because practices don't always hit full revenue from day one. Patient retention during ownership transitions varies. Some patients leave. Referral relationships take time to rebuild. Credentialing with insurance panels can delay reimbursements 60-90 days. The lender's 10% cushion covers loan payments and essential expenses during that adjustment.

The Hidden Costs That Add Up Fast

Where many buyers get surprised: costs outside the purchase price that still require cash at closing or shortly after. Legal fees for contract review typically run $5,000-$15,000 depending on complexity. Loan origination fees often add 1-2% of the total loan amount — on a $700,000 loan, that's $7,000-$14,000. If the practice needs equipment updates, technology upgrades, or minor renovations, those costs land in the first months.

Then there's working capital: money needed to cover payroll, supplies, and operating expenses before revenue stabilizes. Many practices take 3-6 months to return to pre-transition production levels. During that window, you're still paying staff, ordering supplies, covering fixed costs like rent and utilities.

A Realistic Target for Most Buyers

If you're looking at a $700,000 practice, a realistic cash target: $70,000 in lender-required reserves, plus $30,000-$50,000 for working capital, legal fees, loan origination, and transition costs. That brings your total to $100,000-$120,000 in accessible funds before making offers.

Does that feel like a lot? For many associates, it does — especially when student loans and cost of living already stretch monthly budgets. But this number separates buyers who can act quickly when the right practice appears from those who spend months or years waiting to save enough. The buyers who close deals aren't necessarily earning the most — they're the ones who aligned spending with ownership goals early and built liquidity intentionally.

If $100,000 feels unreachable, it's worth asking whether your current financial structure supports ownership at all. That's not a judgment — it's a planning question. Some associates realize they need to increase income, reduce expenses, or delay ownership 12-18 months to hit their target. Others discover that adjusting spending habits or automating savings makes the goal more achievable than assumed.

The cash cushion isn't just a lender requirement. It's the resource that lets you navigate the first year without constant financial stress — and that difference shows up in how you lead the practice, retain staff, and build patient trust from day one.

Sources & References

The data and claims in this article are drawn from the following sources. We prioritize government data, peer-reviewed research, and established industry publications to ensure accuracy.

- How Long Does It Take to Purchase a Dental Practice?— polishedlegal.com

- Entry #21: How Much Money Do I Need in the Bank to Become a ...— www.practicebiopsy.com

Ready to transition from associate to owner?

Buying a dental practice is a significant milestone that requires careful planning and the right support. Minty Plus provides hands-on guidance through every step of the acquisition process, helping you navigate timelines, financing, and post-close management.